Pros & Cons of Financing a Vehicle with a Dealer vs a Credit Union

The average American buys nine vehicles in his or her lifetime. With so much practice, you might think we would figure out how to get a great deal. But many folks don’t take the time to learn how to haggle over auto prices. They also fail to research the best way to pay for the car.Obviously, most consumers don’t walk into dealerships with fists full of cash. They borrow money to purchase that rugged pickup, luxury sedan, stylish SUV or kid-toting minivan. Some get their loans for pre-owned and new cars from banks or credit unions, while others finance through auto dealerships.

So where should you get a car loan? Consumer advocates agree that banks and credit unions almost always offer the best financing choices for cars, motorcycles, RVs, and other vehicles. Not only do they tend to offer lower interest rates and fees, but most will conveniently pre-approve your loan before you head to the dealer.

At the same time, experts are wary of dealer financing, which often involves higher interest rates and inflated fees. The nonprofit Center for Responsible Lending looked at one year’s worth of auto loans and concluded that U.S. consumers who financed through dealers overpaid by nearly $26 billion over the life of those loans. Advocates specifically warned of hidden loan “acquisition fees” that can total more than $2,500 per vehicle.

What to Watch Out For

Sometimes, car dealers can make their offers sound great in the media or online. But often there is more – or less – than meets the eye. One tactic is to lump unwanted extended warranties and insurance products in with dealer financing costs. Another is to offer a low interest rate in order to seal the deal, but later claim that the initial financing “fell through” and the only way the buyer can get the car is to agree to a higher rate.In contrast, financial institutions are required to be transparent about borrowing costs. You can trust the lending department at MECU to clearly state the loan terms and all the associated fees.

Here are other scenarios you might consider:

Scenario 1: You need a car immediately. You want to get the whole task done in one day. So, it seems most convenient to get both the vehicle and loan from one place.

Reality Check: It’s possible to achieve your one-stop goal and still avoid dealer financing. Many banks and credit unions have “preferred dealer” programs. Participating car dealers are listed on the financial institution’s website. When you buy from one of those dealers, tell them you want to finance through your bank or credit union’s program. The dealership will handle the paperwork, and you’ll get fair terms from a lender you trust.

Scenario 2: Dealerships are offering zero percent interest promotions.

Reality Check: Buyer beware! Those offers might be available only for certain car models or for consumers with top-tier credit scores. Even if you qualify, it might be better to accept another promotion that’s often available – a manufacturer’s cash-back deal -- and then finance the vehicle at your bank or credit union. You’re likely to come out ahead with both cash in hand and excellent loan terms.

Scenario 3: A car salesman boasts about how the dealership does business with many financial institutions and can “shop around” to get you the best loan deal.

Reality Check: The reality is that dealers aren’t often motivated to find the lowest interest rate. One way they make money is through commissions paid by various lenders. That means they often push you to accept a loan from a lender that pays the dealer a high commission rather than one that offers low interest rates. A bank or credit union will offer you the best possible rate without you having to haggle for it.

Scenario 4: A dealer touts its willingness to loan money to consumers with poor credit scores.

Reality Check: Many banks and credit unions also offer specific types of loans – with more favorable terms -- to first-time car buyers or consumers with lower credit scores.

Other Advantages

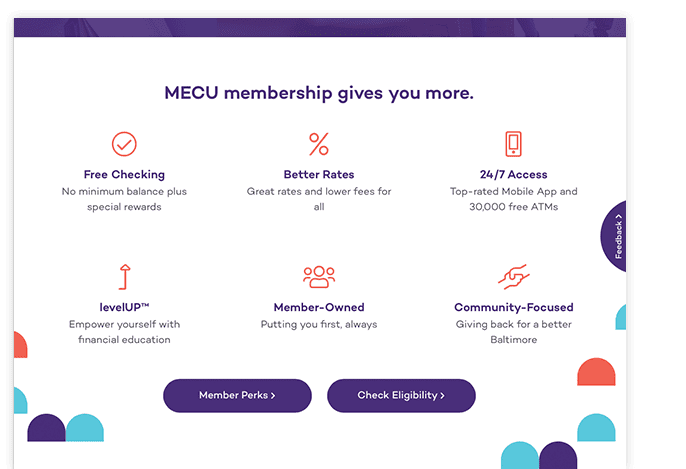

Need a few more reasons why MECU is the best place to get your auto loan?- Many credit unions will pre-approve your loan before you go car shopping, so you know exactly how much you have to spend before negotiating with the dealer. Loan pre-approval can spare you the possible embarrassment of a dealership rejecting your financing application.

- Many credit unions offer interest rate discounts on your auto loan if you have enough money in your other accounts or you agree to make loan payments through automatic monthly deductions from your checking account.

- MECU is a trusted name in your community. When you borrow from us, there’s no danger in doing business with a fly-by-night operation, as might be the case when a dealer farms out your loan to an unknown lender located hundreds of miles away.